Getting Hotter: The Expected Market Time for sellers is dropping like a rock as demand expands.

Eagerly digging through a newly opened box of Cracker Jacks to isolate the treasured prize only to find two prizes, that is unexpected. Standing at the Starbucks cash register ready to pay for a Venti® coffee and the barista explains it has already been paid for by the prior customer, that is unexpected. Receiving a love note from a spouse, or significant other, yet it is not a birthday, anniversary, or holiday, that is unexpected. Surging housing demand amid a pandemic where the overall economy is struggling to come back online, that is unexpected.

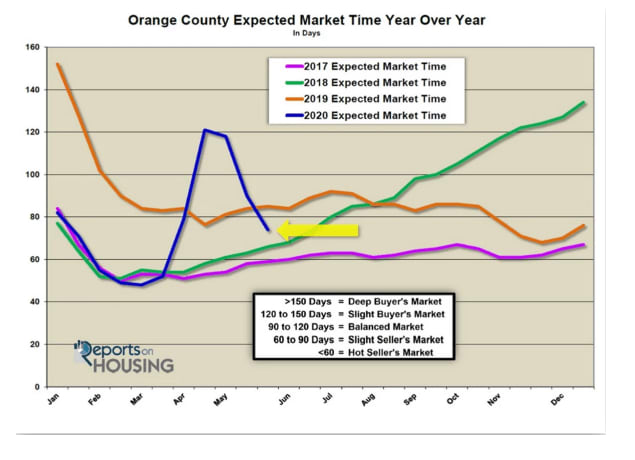

In mid-April, the Expected Market Time (the amount of time from hammering in the for sale sign to opening escrow) was at 121 days, a slight Buyer’s Market (between 120 and 150 days). Since then, it has dropped by 39% and now the Expected Market Time sits at 74 days, a slight Seller’s Market (between 60 and 90 days), totally unexpected. On average, in the past five years, it has increased by 8 days in the same time period. Last year, the Expected Market Time was at 85 days, slower than today.

There are several factors that have led to the quick recovery in housing. First, housing is coming from a position of strength. Since the Great Recession, credit qualification has been extremely tight. Buyers had to go through a rigorous process of proving that they could afford the monthly payment. Homeowners are sitting on a mountain of nested equity as a result of healthy down payments and steady home value appreciation from 2012 through the start of 2020. And, homeowners did not use their homes as piggy banks like they did prior to the Great Recession when they tapped into their equity to pay for everything from lavish European vacations to erasing ballooning credit card debt from rampant, non-essential spending.

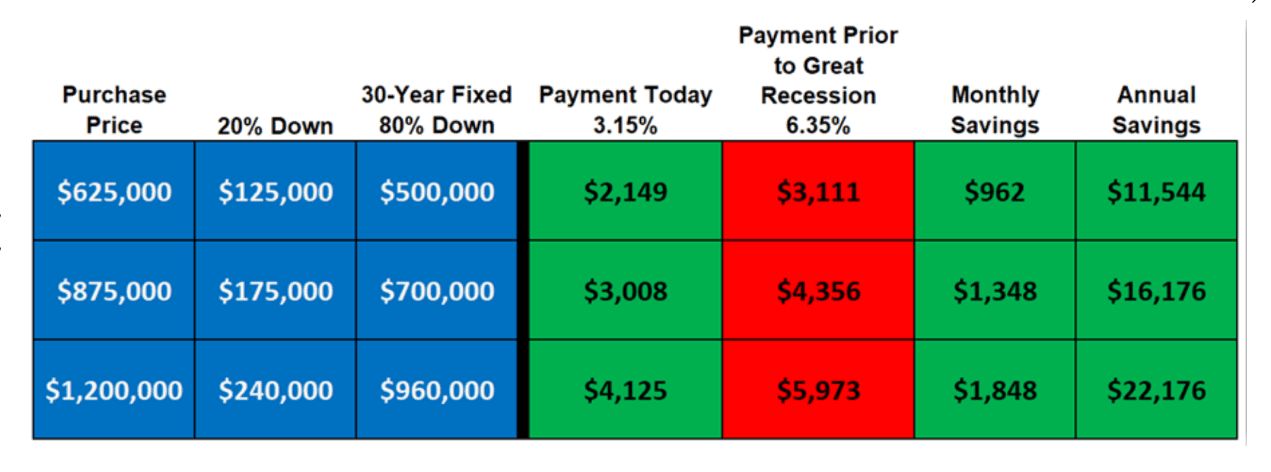

Furthermore, the low mortgage rate environment has enabled homeowners to finance and refinance monthly payments to levels that do not stretch the household budget. And, Freddie Mac just reported that the 30-year mortgage rate across the country just hit another all-time new low, 3.15%. Prior to the Great Recession, mortgage rates were at 6.35%. A $700,000 mortgage payment at 3.15% is $3,008 per month compared to $4,356 per month Prior to the Great Recession in 2007. That is a savings of $1,348 per month, or $16,176 per year. That is an astronomical savings for a family.

It is no wonder that current demand is pumping on all cylinders and has paved the way to a “V-Shaped” recovery. Home affordability has improved dramatically due to record low rates and buyers want to take advantage of this incredible opportunity. As a result, demand (the number of new pending sales over the prior month) in Orange County has increased by 74% in the past four weeks, rising from 1,172 pending sales to 2,035.

"Housing has not just awakened, it is roaring back at an unprecedented level."

It is as if the Spring Market is coming back online. Current demand is now equivalent to the start of February of this year, right after the Super Bowl. That is typically the best time of the year for sellers, between February and mid-May. It is hard to believe that just six weeks ago, in mid-April, demand hit levels not seen since the Great Recession, inherent, anemic demand. The COVID-19 pandemic is losing its impact and grip on demand. It is currently off by only 23% compared to last year, 611 fewer escrows, and the difference is diminishing.

Meanwhile, COVID-19 is also losing its grip on homeowners coming on the market. In the past 4-weeks, 2,763 homes were placed on the market in Orange County. That is 33% less than the five-year average of 4,132. Six weeks ago, it was a 54% difference. As a result, the active inventory has increased from 4,344 homes in mid-April to 5,044 homes today, a 16% rise. Yet, the active inventory remains at its lowest level for an end to May since 2013, the hottest year during the 8-year expansion from 2012 through the start to 2020. And, there were 33% more homes last year, an extra 2,435.

With surging demand and an anemic active inventory, the Expected Market Time dropped like a rock and the market transitioned from one that slightly favors buyers to one that slightly favors sellers. Sellers get to call more of the shots while home values are not changing much at all.

The market is still ramping up and the momentum is palpable. Housing is not only hotter than last year, it is poised to only get stronger, antagonized by record low rates. As the rise in demand continues to outpace any rise in the supply of homes, the Expected Market Time will continue to fall, and housing will line up further in favor of sellers.

For homes that come on the market below $1 million in great condition and priced well, expect multiple offers and a lot of competition. Do not expect

discounting because of COVID-19. At this point it could not be further from the reality of today’s market. Housing has proved to be the industry that is extremely resilient. The laws of supply and demand have paved the way for a rapidly improving housing market. In a multiple offer situation, the buyer who writes the best offer to purchase a home will become the winning bidder. Everybody else will have to go back to the drawing board.

Success ultimately boils down to pricing a home according to its Fair Market Value. Even when the housing market lines up in favor of sellers,

many homeowners become overly confident and price their homes out of bounds, requiring price reductions down the road. For a seller to get top dollar for their home, they have to take advantage of the initial few weeks of coming on the market, which is when a home procures the most activity and exposure. This can only be accomplished through accurate pricing.